Share this article

How Fintech Apps Make Money: 15 Proven Revenue Models

Financial technology, or fintech, has fundamentally changed the way people access banking, invest money, send payments, and manage personal finance. Over the past decade, fintech apps have moved from niche tools to everyday essentials used by billions of people across the globe.

Whether it is a digital wallet that lets you split a restaurant bill in seconds, a robo-advisor that automatically rebalances your portfolio, or a buy-now-pay-later platform that makes large purchases accessible, fintech apps are reshaping how value moves in the modern economy.

What Are Fintech Apps?

Fintech apps are mobile or web-based applications that deliver financial services digitally. They span a wide range of categories, including payments, lending, investing, insurance, personal finance management, cryptocurrency exchanges, and open banking platforms. Unlike traditional financial institutions, fintech apps prioritize speed, accessibility, and user experience.

Why Fintech Is Booming Globally

Several factors are driving the rapid adoption of fintech worldwide. Smartphone penetration has crossed 6.9 billion users globally. Traditional banks continue to underserve large segments of the population in emerging markets. Younger generations prefer digital-first financial services that fit into their daily app ecosystem.

Regulatory innovation, including open banking frameworks in Europe and India’s UPI infrastructure, has further accelerated growth by lowering barriers to entry for new fintech startups.

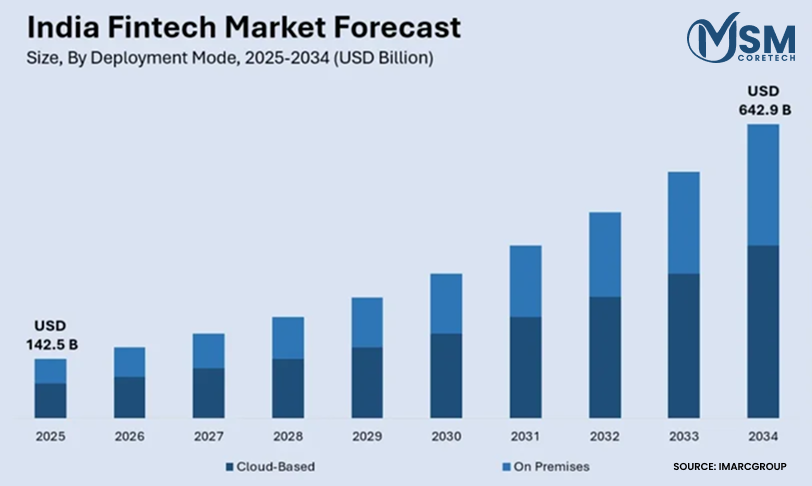

Fintech Market Size and Forecast 2026

India’s fintech market is entering 2026 with strong growth momentum, driven by rising digital adoption and expanding financial access. The market, valued at USD 142.5 billion in 2025, is steadily scaling as more users shift to digital financial services. With consistent innovation and policy support, the sector is set for long-term expansion.

- Projected to reach USD 642.9 billion by 2034 at a CAGR of 16.7%

- UPI continues to dominate digital payments across the country

- Rapid growth in digital lending, embedded finance, and wealth tech

- Increasing adoption in tier-2 and tier-3 cities boosting market reach

Why Understanding Fintech Monetization Is Critical

Building a fintech app with great features is only half the equation. The other half is understanding how your product will generate sustainable revenue. Many early-stage fintech startups raise significant funding, build polished user interfaces, and acquire hundreds of thousands of users, only to discover later that their monetization strategy is insufficient to sustain operations.

The Growth vs Profitability Problem

In fintech, growth and profitability are often in direct tension. To attract users quickly, apps offer free services, cashback rewards, and zero-fee transactions. While this drives adoption, it also defers revenue generation. The challenge is knowing precisely when and how to introduce monetization without causing user churn.

Companies like Robinhood and Chime scaled aggressively on free models before layering in revenue streams. Replicating this strategy without a clear path to profitability is one of the most common strategic errors in fintech.

Investor Expectations

Fintech investors in 2025 are more demanding than ever. Post the 2022 funding correction, venture capital firms are now scrutinising unit economics, customer acquisition cost (CAC), lifetime value (LTV), and churn rates far more rigorously. Founders who cannot clearly articulate their monetization roadmap will struggle to raise subsequent rounds.

Having a clearly defined and diversified revenue model is now a prerequisite, not an afterthought, for fintech fundraising.

Why Many Fintech Apps Struggle to Make Money

The most common monetization mistakes in fintech include over-reliance on a single revenue stream, misalignment between the target user segment and the chosen revenue model, building features that users enjoy but are not willing to pay for, and underestimating the regulatory costs associated with financial services.

Understanding proven monetization strategies before writing a single line of code gives your fintech product a structural advantage from day one.

How Do Fintech Apps Make Money? (Quick Overview)

Fintech apps make money by integrating one or more revenue models into their product architecture. Unlike traditional software, fintech monetization is deeply tied to financial transactions, user behaviour, and regulatory permissions. The most successful fintech companies use multiple revenue streams simultaneously, reducing dependence on any single source and maximising lifetime value per user.

The core principle is straightforward: every interaction a user has within the app, whether sending money, investing, borrowing, or spending, presents a potential monetization opportunity. The art lies in designing these touchpoints so they feel valuable to the user while generating revenue for the platform.

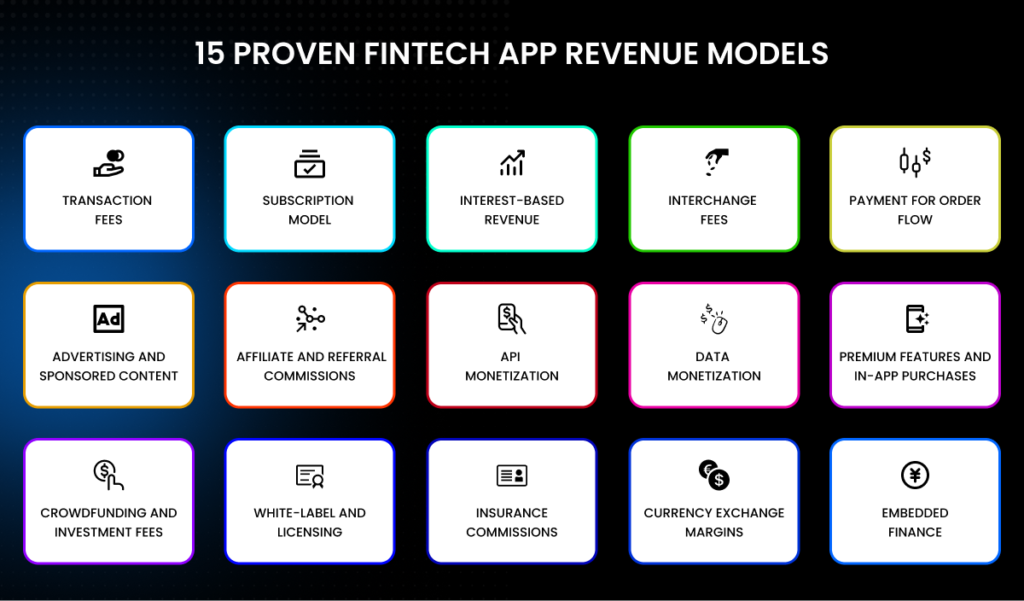

Below, we explore 15 proven revenue models that are actively being used by the world’s most profitable fintech applications.

15 Proven Fintech App Revenue Models

1. Transaction Fees

Transaction fees are the most fundamental revenue model in fintech. Every time a user initiates a payment, transfer, or financial transaction, the platform charges a small percentage or flat fee. Payment processors like Stripe charge 2.9 percent plus $0.30 per transaction, while international remittance platforms charge a percentage of the transferred amount.

This model works particularly well for payment apps, digital wallets, and cross-border transfer services. The key advantage is that revenue scales automatically with user activity. As your user base grows and transaction volume increases, revenue grows proportionally without requiring additional product investment.

Best suited for: payment wallets, P2P transfer apps, e-commerce payment gateways, and point-of-sale fintech solutions.

2. Subscription Model (Freemium to Premium)

The subscription model is one of the most predictable and scalable revenue streams in fintech. Apps offer a free tier with basic features and then charge a monthly or annual fee for access to premium capabilities. This approach, known as freemium, allows users to experience value before committing financially.

Premium subscription features often include higher transaction limits, advanced analytics dashboards, priority customer support, exclusive investment tools, and international transfer discounts. Robinhood Gold, for example, charges a monthly fee that unlocks margin investing, larger instant deposits, and professional research reports.

Subscription tiers should be designed so that the free tier is genuinely useful, the premium tier is aspirational, and the upgrade trigger is naturally encountered during normal app usage.

3. Interest-Based Revenue (Lending and BNPL)

Lending-based fintech apps generate revenue by charging interest on loans, credit lines, or buy-now-pay-later (BNPL) installments. This is one of the highest-margin revenue models in fintech when managed with robust credit risk assessment.

BNPL platforms like Affirm and Klarna allow users to split purchases into zero-interest or low-interest installments while charging merchants a fee and earning interest from users who extend repayment periods. Personal lending apps and digital credit lines charge annual percentage rates (APR) that vary based on user credit scores and loan tenure.

For this model to work profitably, the fintech company must invest in advanced risk scoring, fraud detection, and regulatory compliance. The margin potential is high, but so are the operational costs.

4. Interchange Fees (Card Payments)

When a user swipes a debit or credit card issued by a fintech platform, the merchant’s bank pays an interchange fee to the card-issuing bank. Neobanks and digital banking apps that issue their own cards earn a share of this interchange fee on every transaction.

Chime, one of the most well-known US neobanks, generates the majority of its revenue from interchange fees. The model is elegant because it monetizes user behaviour that is already happening naturally. Users spend money; the platform earns a small percentage every time they do.

Visa and Mastercard interchange rates typically range from 0.3 to 2 percent depending on the transaction type and card tier.

5. Payment for Order Flow (Trading Apps)

Payment for order flow (PFOF) is a model used by trading and investment apps where the platform routes user trade orders to specific market makers in exchange for compensation. Robinhood popularized this model by offering commission-free stock trading and earning revenue from market makers who executed the orders.

PFOF has attracted regulatory scrutiny in several markets, particularly in the EU where it has been restricted. However, it remains a legitimate and highly profitable model in the United States for platforms with significant trading volume.

6. Advertising and Sponsored Content

Fintech apps with large, highly engaged user bases can monetize through targeted advertising and sponsored financial product placements. Credit Karma, a personal finance platform with over 130 million members, generates significant revenue by displaying personalized offers for credit cards, loans, and insurance products from financial partners.

Unlike generic display advertising, fintech advertising is highly contextual. A user who just checked their credit score is a highly qualified lead for a credit card offer. This contextual relevance makes fintech advertising inventory far more valuable than typical mobile advertising.

This model works best when combined with strong first-party data and user consent frameworks to remain compliant with data privacy regulations.

7. Affiliate and Referral Commissions

Fintech apps act as distribution channels for financial products by earning referral commissions when users sign up for partner services such as bank accounts, credit cards, insurance policies, or investment products. Comparison platforms like NerdWallet and MoneySuperMarket earn hundreds of millions in annual revenue through affiliate commissions.

For mobile fintech apps, this model is often implemented through in-app product recommendations, personalized financial advice engines, or partner offer sections. The commission structure varies: some pay per lead, others pay per successful account opening, and some offer revenue sharing for the lifetime of the customer.

8. API Monetization (Open Banking)

Open banking has created an entirely new category of fintech revenue: API monetization. Platforms that aggregate financial data, facilitate bank connections, or provide financial infrastructure can charge third-party developers and businesses for access to their APIs.

Plaid, the financial data network, charges businesses a fee every time their customers connect a bank account through Plaid’s API. This B2B revenue model is highly scalable and benefits from strong network effects: the more banks and financial institutions are connected, the more valuable the platform becomes.

For fintech apps with proprietary financial infrastructure or unique data assets, API monetization represents a high-margin revenue layer that operates largely independently of the consumer-facing product.

9. Data Monetization (Privacy-Compliant)

Aggregated and anonymized financial behaviour data is enormously valuable to retailers, financial institutions, research firms, and marketing companies. Fintech apps that process large volumes of transaction data can monetize these insights while remaining compliant with GDPR, CCPA, and other data privacy regulations.

It is critical that any data monetization strategy is built on explicit user consent, robust anonymization processes, and transparent data governance policies. When done ethically and transparently, data monetization can contribute a meaningful percentage of total revenue without compromising user trust.

10. Premium Features and In-App Purchases

Beyond full subscription tiers, fintech apps can monetize specific premium features as standalone purchases or unlockable add-ons. These might include advanced portfolio analysis tools, tax optimization reports, spending insights dashboards, or exclusive access to investment opportunities.

This granular approach to monetization allows users to pay only for features they genuinely value, reducing the psychological barrier of a full subscription commitment while still driving revenue from highly engaged users.

11. Crowdfunding and Investment Fees

Equity crowdfunding and investment platforms charge platform fees on every successful capital raise. Platforms like Seedrs and Republic charge a percentage of the total amount raised, plus an annual management fee on subsequent returns. Some platforms also charge investors a carry percentage on profitable exits.

This model is highly lucrative but requires significant regulatory compliance investment, including financial licenses, KYC/AML processes, and investor suitability assessments.

12. White-Label and Licensing

Fintech companies with proven technology infrastructure can license their platform to other businesses and financial institutions. White-label banking platforms, payment processing engines, and compliance technology solutions are sold as B2B SaaS products with annual license fees or revenue-sharing arrangements.

This is a capital-efficient revenue model because the same technology developed for the consumer product can be packaged and sold multiple times without proportional additional investment. Companies like Mambu and Thought Machine generate substantial revenue by licensing their core banking software to banks worldwide.

13. Insurance Commissions

Neobanks, personal finance apps, and travel fintech platforms often integrate insurance product recommendations, earning referral commissions from insurance providers for every policy sold through their platform. Revolut, for example, offers travel insurance, phone insurance, and medical cover as add-on services within its banking app.

As embedded insurance (insurtech) grows, fintech apps are increasingly becoming primary distribution channels for insurance products, earning significant commission revenue without taking on underwriting risk.

14. Currency Exchange Margins

International remittance and multi-currency wallet apps generate revenue by applying a small margin on top of the interbank exchange rate when users convert currencies. Wise (formerly TransferWise) built a multi-billion dollar business by offering exchange rates significantly better than traditional banks while still earning a transparent fee on each conversion.

The currency exchange margin model is particularly effective in high-remittance corridors such as US to Mexico, UK to India, and UAE to Pakistan, where transaction volumes are enormous and traditional bank fees are disproportionately high.

15. Embedded Finance

Embedded finance is the fastest-growing monetization trend in fintech. It involves integrating financial services, including payments, lending, insurance, and investment products, directly into non-financial platforms such as e-commerce stores, ride-sharing apps, and HR software.

Shopify earns revenue by offering Shopify Capital loans to merchants directly within its platform. Uber provides driver financial services through an embedded banking product. In both cases, the platform earns revenue by acting as the distribution layer for financial services without being a licensed financial institution itself.

For fintech developers, embedded finance represents an enormous opportunity to build revenue-generating infrastructure that powers third-party platforms at scale.

Fintech Revenue Models Comparison Table

The table below provides a structured comparison of all 15 fintech revenue models, helping founders and product teams quickly identify which model best aligns with their app type, target audience, and growth stage.

| Revenue Model | Revenue Type | Best For | Profit Potential | Example Apps |

|---|---|---|---|---|

| Transaction Fees | Per transaction cut | Payment apps | Medium | PayPal, Stripe |

| Subscription (Freemium) | Recurring monthly/annual | SaaS fintech | Medium-High | Robinhood Gold, YNAB |

| Interest-Based (Lending/BNPL) | Interest on loans/EMI | Loan and BNPL apps | High | Affirm, Klarna |

| Interchange Fees | Card swipe fee share | Neobanks | Medium | Chime, Revolut |

| Payment for Order Flow | Broker routing fees | Trading apps | Medium | Robinhood |

| Advertising | CPM / sponsored content | Free consumer apps | Low-Medium | Credit Karma |

| Affiliate/Referral | Commission per lead | Comparison platforms | Medium | NerdWallet |

| API Monetization | API call fees | Open banking | Medium-High | Plaid, MX |

| Data Monetization | Anonymised insights sold | Large-scale apps | High (regulated) | Credit bureaus |

| Premium In-App Features | One-time / recurring | Freemium apps | Medium | Acorns, Mint |

| Crowdfunding/Investment Fees | Platform % of raise | Investment platforms | High | Seedrs, Republic |

| White-Label / Licensing | SaaS licensing fees | B2B fintech | High | Mambu, Thought Machine |

| Insurance Commissions | Referral from insurer | PFM / neobanks | Medium | Revolut, Lemonade |

| Currency Exchange Margins | Spread on FX rates | Remittance apps | Medium-High | Wise, Western Union |

| Embedded Finance | Revenue share from BaaS | Non-fintech platforms | High | Shopify, Uber |

How Popular Fintech Apps Make Money

Understanding how market-leading fintech companies have structured their revenue models provides valuable blueprints for new entrants. Below are three in-depth breakdowns of how globally recognised fintech apps generate revenue.

PayPal

PayPal is one of the original fintech success stories and remains one of the most profitable payment platforms in the world. Its primary revenue source is transaction fees charged to merchants for processing payments, typically around 2.9 percent plus a fixed fee per transaction. PayPal also earns revenue from its Venmo platform through business profile fees, instant transfer charges, and the Venmo credit card. Additionally, PayPal Capital, its small business lending product, generates interest income, while its international operations benefit from currency conversion margins.

Robinhood

Robinhood disrupted the brokerage industry by offering commission-free stock trading, but its revenue model is more sophisticated than it appears. The largest revenue stream is payment for order flow, where market makers pay Robinhood for routing trade orders through their systems. Robinhood Gold, a premium subscription at approximately nine dollars per month, adds recurring revenue. The platform also earns interest on uninvested cash held in user accounts, stock lending fees, and interchange revenue from its debit card.

Chime

Chime is a US neobank that built a multi-billion dollar valuation primarily on interchange fee revenue. Every time a Chime user swipes their Visa debit card, Chime earns a small percentage of the merchant fee. Given that Chime has over 22 million account holders with highly active spending habits, this adds up to hundreds of millions in annual revenue. Chime supplements this with credit builder card revenue and out-of-network ATM fees.

Case Study: Revenue Breakdown of a Fintech App

To illustrate how multiple revenue streams work together in practice, let us examine a hypothetical mid-sized fintech app serving 500,000 active users in a competitive market. This example is representative of the revenue architecture used by many successful fintech startups in their second and third years of operation.

Example User Journey

A user discovers the app through a social media advertisement (acquisition cost: USD 18). They sign up for free, connect their bank account, and begin using the payment and budgeting features. After three months, they hit the free tier transaction limit and upgraded to the premium subscription. Six months later, they apply for a credit line directly within the app. Two years after signup, they are a highly profitable user across three separate revenue streams.

Revenue Flow Breakdown

| Revenue Stream | % of Total Revenue | Monetization Trigger |

|---|---|---|

| Transaction Fees (payment processing) | 35% | Every completed transaction |

| Subscription (Premium tier) | 28% | User upgrades after hitting free limit |

| Interchange Fees (debit card) | 15% | Every card swipe at merchant |

| Lending Interest (BNPL / credit line) | 12% | User opts into EMI or credit |

| Affiliate Commissions | 7% | User clicks and converts via partner offer |

| API Access (B2B) | 3% | Third-party developers integrate the API |

This diversified revenue architecture means the company is not disproportionately dependent on any single stream. If transaction volumes drop seasonally, subscription and lending revenue provide a stable base. This is precisely the kind of resilient monetization structure that sophisticated investors look for.

Advanced Monetization Strategies Used by Fintech Apps

AI-Driven Monetization

Artificial intelligence is enabling a new generation of fintech monetization strategies. AI models can analyse user spending patterns, predict when a user is most likely to need credit, and proactively surface relevant product offers at precisely the right moment. This contextual intelligence dramatically increases conversion rates on premium features and partner product recommendations.

AI-powered credit scoring enables fintech lenders to approve users who would be declined by traditional models, expanding the addressable lending market while managing risk more accurately. Companies that invest in proprietary AI models gain a compounding competitive advantage as their models improve with more data over time.

Behavioural Pricing

Behavioural pricing uses insights from user behaviour, transaction history, and financial profile to offer personalised pricing. Rather than a single subscription price for all users, a fintech app might offer the same premium tier at different price points based on the user’s location, income level, or willingness to pay signals. This dynamic approach to pricing can meaningfully increase average revenue per user (ARPU) without sacrificing conversion rates among price-sensitive segments.

Dynamic Pricing

Dynamic pricing adjusts fee structures in real time based on market conditions, liquidity, transaction risk, or platform load. Currency exchange apps, for example, adjust their margin dynamically based on interbank rate volatility. Lending apps may adjust interest rates based on real-time credit risk assessments. Dynamic pricing requires sophisticated backend infrastructure but can significantly optimise revenue per transaction.

Embedded Finance Ecosystems

The most sophisticated fintech monetization strategy involves building an embedded finance ecosystem where the platform becomes the infrastructure layer for multiple other products and businesses. By opening APIs to third-party developers and embedding financial services into non-financial applications, fintech companies can create network effects that generate revenue across an entire ecosystem rather than just from direct users.

How to Choose the Right Monetization Strategy

Based on App Type

The nature of your fintech product should be the primary driver of your monetization strategy. Payment apps naturally align with transaction fees. Investment platforms are better suited to subscription or PFOF models. Lending apps should prioritise interest revenue. Trying to force an incompatible model onto a product type will result in poor user experience and low conversion rates.

Based on User Behaviour

Study how your users actually interact with your app. What features do they use most frequently? At what point in their journey do they derive the most value? These insights should directly inform where you place monetization triggers. If users are highly active daily transactors, a transaction fee model will generate more revenue than a monthly subscription. If users primarily use the app for occasional large transfers, a flat fee per transaction makes more sense than a percentage-based model.

Based on Region

Fintech monetization is heavily influenced by regional factors including income levels, regulatory frameworks, and competitive dynamics. In India, for example, the UPI payment system has made transaction fees on domestic payments nearly impossible. Fintech apps in India must therefore rely more heavily on lending, subscriptions, or insurance commissions. In Europe, open banking regulations enable strong API monetization opportunities. In the United States, PFOF and interchange remain viable and profitable.

Fintech Monetization Strategy Framework

A structured monetization framework helps fintech founders move beyond guesswork and build revenue models that are intentional, measurable, and scalable.

User Segmentation

Begin by segmenting your users based on financial behaviour, transaction frequency, income level, and product engagement depth. Different segments will respond differently to various monetization approaches. High-frequency transactors are ideal targets for transaction fee models. Financially sophisticated users are more likely to convert on premium investment tools. Underserved credit segments are the target for lending products.

Pricing Tiers

Design your pricing tiers so each level delivers clear, tangible value over the one below it. The free tier should solve a real problem well. The first paid tier should provide features that power users genuinely need. The top tier should serve business or professional users with enterprise-grade capabilities. Avoid creating tiers that feel arbitrary or where the value jump between levels is unclear.

Revenue Triggers

Revenue triggers are the specific in-app moments that prompt users to convert or transact. Examples include hitting a free tier usage limit, completing a large transaction that surfaces a premium feature recommendation, or receiving an AI-generated insight that requires a paid upgrade to act on. Intentionally designing these moments into your product flow is one of the most effective ways to increase monetization rates without feeling aggressive or intrusive.

Fintech Revenue Calculator (Lead Magnet)

Use the following framework to estimate your fintech app’s potential annual revenue. This is a simplified model for planning purposes and should be adjusted based on your specific market, unit economics, and conversion data.

Transaction Fee Revenue: Monthly Active Users x Average Monthly Transactions per User x Average Transaction Value x Fee Percentage x 12 months

Subscription Revenue: Monthly Active Users x Freemium-to-Paid Conversion Rate x Monthly Subscription Price x 12 months

Lending Revenue: Active Borrowers x Average Loan Size x Annual Interest Rate x Repayment Period Factor

Example Calculation for a 500,000 MAU Payment App:

- Transaction fees: 500,000 users x 8 transactions x USD 50 x 1.5% x 12 = USD 36,000,000

- Subscription (5% conversion at USD 9.99/month): 25,000 x USD 9.99 x 12 = USD 2,997,000

- Affiliate commissions (2% conversion at USD 45 CPA): 10,000 conversions x USD 45 = USD 450,000

- Total estimated annual revenue: approximately USD 39.4 million

These numbers will vary significantly based on your market, user engagement levels, and competitive pricing. Use this as a starting point for your financial modelling.

Hidden Costs That Impact Fintech Profitability

Gross revenue is only part of the profitability story. Fintech companies face a range of operational costs that are often underestimated at the planning stage. Understanding these costs is essential for accurate margin forecasting and realistic investor projections.

| Cost Category | Typical Annual Range (USD) | Impact on Margins |

|---|---|---|

| Regulatory Compliance & Licensing | $50,000 – $500,000+ | High |

| Fraud Prevention Systems | $30,000 – $200,000 | Medium-High |

| Cloud Infrastructure & Scaling | $20,000 – $300,000 | Medium |

| Customer Acquisition Cost (CAC) | $15 – $200 per user | High (early stage) |

| Security Audits & Penetration Testing | $20,000 – $100,000 | Medium |

| Payment Gateway Fees (third-party) | 1.5% – 3.5% per txn | Medium |

Compliance and Legal Costs

Fintech is one of the most heavily regulated industries in the world. Depending on your product category and operating jurisdiction, you may need payment processing licenses, money transmitter licenses, lending licenses, investment adviser registration, or cryptocurrency exchange approvals. Legal fees for obtaining and maintaining these licenses can range from tens of thousands to several hundred thousand dollars annually.

Fraud Prevention Systems

Financial apps are high-value targets for fraudsters. Robust fraud prevention infrastructure, including real-time transaction monitoring, device fingerprinting, velocity checking, and machine learning-based anomaly detection is not optional. The cost of fraud losses and chargebacks without these systems far exceeds the investment in prevention.

Infrastructure and Scaling

Fintech apps must maintain extremely high availability standards, often targeting 99.99 percent uptime. Financial transactions cannot fail due to infrastructure outages. Cloud infrastructure costs scale rapidly as user numbers grow, and the need for geographic redundancy, disaster recovery systems, and real-time processing capabilities adds significant ongoing expenses.

Customer Acquisition Cost (CAC)

Acquiring fintech users is expensive. Paid digital advertising, influencer partnerships, referral bonuses, and promotional cashback offers all contribute to high CAC figures, particularly in competitive markets. The key to profitability is ensuring that the lifetime value (LTV) of each acquired user significantly exceeds the cost of acquiring them, typically targeting an LTV to CAC ratio of at least 3 to 1.

Post-Launch Costs and Maintenance

App Updates and Improvements

Financial technology evolves rapidly. User expectations are set by the best products in the market. Maintaining a competitive app requires continuous investment in feature development, UI improvements, performance optimization, and the integration of new financial services. Budgeting for ongoing development at roughly 20 to 30 percent of the initial build cost annually is a reasonable starting point.

Server Scaling

As transaction volumes grow, server infrastructure must scale proportionally. Cloud-based auto-scaling solutions help manage costs by provisioning resources dynamically, but unexpected traffic spikes, particularly during financial market volatility or viral growth moments, can result in significant unplanned infrastructure spending.

Security Updates

Financial applications are subject to a constant stream of security threats. Regular security patches, dependency updates, penetration testing, and code audits are non-negotiable operational requirements. Many jurisdictions require annual security assessments as a condition of maintaining financial licenses.

Challenges in Monetizing Fintech Apps

Low Initial Margins

Most fintech monetization models take time to build meaningful revenue. Transaction fees generate modest income per transaction. Subscriptions take months to build a base. Lending revenue requires capital deployment before interest flows. Early-stage fintech companies should plan for an extended period of negative cash flow while building the user base and transaction volume necessary to make unit economics work.

User Trust Issues

Financial apps handle sensitive personal and financial data. Users are understandably cautious about sharing bank account credentials, social security numbers, and financial history with a startup they discovered six months ago. Building trust takes time, transparency, and a demonstrable commitment to data security and customer service. Monetization strategies that feel extractive or opaque will accelerate churn among trust-sensitive users.

Regulatory Barriers

Regulatory requirements differ dramatically across jurisdictions and product categories. A lending feature that is straightforward to implement in one country may require years of regulatory approval in another. Compliance costs, along with the operational complexity of managing different regulatory requirements across multiple markets, are significant challenges for fintech companies pursuing international growth.

Why Many Fintech Apps Fail to Make Money

Despite the enormous market opportunity, a significant number of fintech apps fail to achieve commercial sustainability. The most common reasons are not technical; they are strategic.

- Weak monetization strategy: Building a product with no clear path to revenue, assuming that scale alone will create monetization opportunities.

- Over-dependence on a single revenue stream: When that stream is disrupted by regulation, competition, or market changes, the entire business model collapses.

- Poor user experience in monetized features: Placing monetization in ways that interrupt natural workflows or feel punitive creates resentment rather than conversion.

- Misaligned pricing: Charging too much too early drives away users before they have experienced sufficient value; charging too little prevents the business from becoming viable.

- Ignoring unit economics: Scaling a business where CAC exceeds LTV simply burns more capital with each new user acquired.

How Much Revenue Can a Fintech App Generate?

Revenue Examples

Revenue potential varies enormously based on the monetization model, user base size, and engagement depth. Small independent fintech apps with 50,000 monthly active users might generate USD 500,000 to USD 2 million annually. Mid-sized platforms with 500,000 users can target USD 10 million to USD 50 million in annual revenue. Enterprise-scale fintech platforms with millions of users, such as PayPal, Stripe, and Robinhood, generate hundreds of millions to billions annually.

Profit Margins

Gross margins in fintech vary significantly by model. Subscription software fintech businesses can achieve gross margins of 70 to 85 percent. Transaction fee models typically achieve 30 to 50 percent gross margins after payment network fees and infrastructure costs. Lending businesses have lower gross margins but benefit from higher absolute revenue per user. A well-diversified fintech platform can target blended gross margins of 50 to 65 percent at scale.

Scaling Potential

One of the most attractive characteristics of fintech business models is their scalability. Unlike traditional financial services businesses that require physical branches and large frontline workforces, fintech platforms can serve millions of users with relatively small teams. Technology infrastructure costs grow sub-linearly relative to revenue as user numbers increase, creating improving margins at scale.

ROI Breakdown of Fintech Apps

Cost vs Revenue Timeline

A typical fintech app investment timeline looks as follows. In months one through six, the focus is on product development, regulatory setup, and soft launch. Revenue is minimal; costs are high. In months seven through twelve, the app enters growth mode. Marketing spend increases, the user base grows, and the first meaningful revenue begins to appear. From year two onward, assuming strong retention and effective monetization, the business begins approaching profitability as operational leverage kicks in.

Break-Even Analysis

Break-even timing depends heavily on the chosen monetization model and initial investment. A bootstrapped fintech app with a lean team and a subscription model might break even within 18 to 24 months. A venture-backed platform pursuing aggressive growth with a transaction fee model might invest several million dollars before generating a positive unit economics quarter. Founders should model multiple break-even scenarios across conservative, base, and optimistic user growth assumptions.

Future Trends in Fintech Monetization

AI and Automation

Artificial intelligence will fundamentally reshape fintech monetization over the next five years. AI-powered personalisation will enable hyper-targeted product recommendations that dramatically improve conversion rates. Automated financial advice engines will create new subscription product categories. AI-driven credit decisioning will expand lending markets to previously unserved populations. Fintech companies that build AI capabilities as a core competency will have significant monetization advantages over those that rely on generic models.

Web3 and Blockchain

Decentralised finance (DeFi) protocols are creating entirely new monetization models based on liquidity provision, yield farming, staking rewards, and protocol fees. While DeFi remains volatile and speculative, the infrastructure being built will eventually underpin mainstream fintech products. Tokenised assets, programmable money, and blockchain-based identity verification will open new revenue opportunities for fintech companies willing to invest in Web3 capabilities.

Embedded Finance

Embedded finance will continue to be the dominant growth trend in fintech monetization. Every major technology platform, from e-commerce to HR software to logistics management, will eventually offer financial services to its users. The companies that build the infrastructure powering these embedded finance integrations will capture disproportionate value. Fintech companies should evaluate both sides of this opportunity: building embedded finance products for their own users and providing infrastructure for other platforms to embed financial services.

How to Build a Profitable Fintech App

Start With MVP

The most successful fintech apps start with a narrowly focused minimum viable product that solves a specific, high-frequency financial problem exceptionally well. Resist the temptation to build a comprehensive financial super-app from day one. Prove product-market fit, validate monetization assumptions, and iterate based on real user data before expanding the feature set.

Choose Scalable Monetization

Select revenue models that improve in unit economics as your user base grows. Subscription and API monetization improve with scale. Transaction fee models benefit from volume. Avoid revenue models that require proportional headcount increases to scale, such as high-touch advisory services, unless you are intentionally targeting a premium segment.

Optimize Conversion Funnel

Map every step of your user journey from initial download to first paid action. Identify where users drop off, where they get confused, and where the value proposition breaks down. Continuously test and optimise the conversion funnel for premium features, subscription upgrades, and lending product adoption. A 10 percent improvement in freemium-to-paid conversion can double revenue without acquiring a single additional user.

Why Hire a Fintech App Development Company

Benefits

Building a fintech app in-house requires assembling a multidisciplinary team with expertise in mobile development, backend architecture, financial APIs, security engineering, compliance, and UX design. This is a complex, expensive, and time-consuming process, particularly for founding teams whose strength lies in financial product strategy rather than technology execution.

A specialist fintech app development company brings pre-built experience across all of these domains. They have built and launched multiple financial products, understand the technical requirements of financial regulatory compliance, have established relationships with payment processors and banking APIs, and can deliver a production-ready, secure fintech application significantly faster than an in-house team starting from scratch.

Cost vs In-House Development

The all-in cost of building an in-house fintech development team for a 12-month project, including salaries, benefits, recruitment costs, and overheads, typically exceeds USD 500,000 to USD 1.5 million depending on location and team size. Engaging a specialist fintech development agency for the same scope typically costs USD 80,000 to USD 350,000 and delivers a faster time to market, lower risk, and access to battle-tested infrastructure and reusable components.

Why Choose MSM Coretech for Fintech Mobile App Development

When it comes to building revenue-generating fintech applications that are secure, scalable, and compliant, MSM Coretech stands out as a trusted development partner for startups, scale-ups, and enterprise financial institutions alike.

MSM Coretech specialises in end-to-end fintech mobile app development, covering everything from initial product strategy and revenue model design to full-stack development, third-party API integration, security architecture, and post-launch growth optimisation. The team brings deep domain expertise in payment systems, lending platforms, investment apps, neobanking solutions, and open banking integrations.

Here is why fintech founders and product teams choose MSM Coretech as their development partner:

Fintech-First Expertise

MSM Coretech has delivered fintech solutions across payment processing, BNPL, digital lending, wealth management, and insurance technology verticals. The team understands the unique technical and regulatory challenges of financial application development.

Revenue-Centric Architecture

Every product MSM Coretech builds is designed with monetization in mind from the architecture level. The team works with founders to map revenue triggers directly into the product flow, ensuring that monetization feels natural rather than forced.

Security and Compliance Built In

Financial applications cannot afford security vulnerabilities. MSM Coretech follows industry best practices including PCI-DSS compliance readiness, end-to-end encryption, biometric authentication, real-time fraud detection integration, and GDPR-compliant data architecture.

Rapid Time to Market

With pre-built fintech components, established API integrations with leading payment providers and banking infrastructure platforms, and agile delivery processes, MSM Coretech delivers production-grade fintech applications significantly faster than typical development timelines.

Scalable Technology Stack

Applications built by MSM Coretech are engineered to scale from 1,000 to 10 million users without requiring fundamental architectural changes. Cloud-native infrastructure, microservices architecture, and auto-scaling capabilities are standard in every delivery.

Post-Launch Partnership

MSM Coretech provides ongoing support, feature development, performance monitoring, and security updates after launch. The relationship does not end at delivery; it continues as your user base grows and your monetization strategy evolves.

Transparent Communication

MSM Coretech operates with full transparency on timelines, costs, and technical decisions. Founders receive regular progress updates, clear documentation, and complete ownership of all code and intellectual property upon project completion.

Whether you are building a fintech app from scratch, modernizing a legacy financial platform, or adding a new revenue stream to an existing product, MSM Coretech has the expertise, infrastructure, and track record to deliver results. Get in touch with the MSM Coretech team today to discuss your fintech project and receive a detailed technical roadmap and cost estimate.

Conclusion

The question of how fintech apps make money does not have a single answer. The most successful fintech businesses build diversified revenue architectures that combine multiple complementary streams, reducing risk while maximizing the revenue potential from each user interaction.

From transaction fees and interchange revenue to subscription models, lending interest, API monetization, and embedded finance, the landscape of fintech monetization strategies is richer and more sophisticated than ever before. Understanding these models deeply, selecting the right combination for your product and market, and building monetization into the core of your product architecture from day one are the foundations of building a profitable fintech business.

The fintech opportunity is enormous, the technology has never been more accessible, and the user appetite for better financial products has never been stronger. The companies that succeed will be those that combine excellent product experiences with intelligent, user-aligned monetization strategies.

Ready to build a fintech app that generates real, sustainable revenue? MSM Coretech is a specialist fintech app development company with the expertise, infrastructure, and track record to bring your vision to market. Contact the MSM Coretech team today to schedule a free discovery call, receive a technical assessment of your idea, and get a detailed project roadmap tailored to your monetization goals.

FAQs

Many fintech apps monetize without direct user fees by earning interchange revenue from card transactions, generating interest income on pooled user deposits, selling aggregate data insights to enterprise clients, or earning referral commissions from financial product partners.

Lending-based revenue consistently generates the highest margins in fintech when paired with strong risk management. Interest income on loans and BNPL arrangements can produce net interest margins of 10 to 25 percent, far exceeding what is achievable with transaction fees or subscription revenue.

Yes, many fintech apps are highly profitable, but profitability typically takes three to five years to achieve for VC-backed companies that prioritize growth.

Payment apps earn money through a combination of transaction fees charged to merchants or users, currency conversion margins on international transfers, premium subscription fees for faster transfers and higher limits, interest income from holding user balances, and cross-sell commissions from financial products offered within the platform.

An interchange fee is a payment made between banks each time a card transaction is processed. When a consumer uses a debit or credit card, the merchant’s bank pays a fee to the card-issuing bank.

Related Posts

Customer-Facing Apps: Examples, Benefits, and Challenges

Your customer woke up this morning, checked three apps before getting out of bed, ordered coffee through a fourth, and...

Read More

How Does Zelle Make Money? Business Model and Revenue Strategy Explained

Instant digital payments have reshaped how people send and receive money in the United States. In a market crowded with...

Read More

Top 10 Food Delivery Apps in 2026

The way people order food has completely changed over the past few years. With the rise of smartphones and internet...

Read More